2016 Energy Markets in Review

By almost every measure, energy market activity in 2016 was not eventful. Through the majority of the year (first 9 months), markets were characterized by a lack of volatility in both the index and forward markets. In Q4 2016, forward market volatility returned, although the increase in volatility is relative (markets remain low) and did not persist.

Why the modest volatility this past December? Market volatility in Q4 was likely the result of cooler temperatures which occurred after a long, warm Fall. As we posted back in November, after citing research from a Seeking Alpha risk manager,

…deviations from normal heating and cooling degree days explain monthly percentage pricing changes.

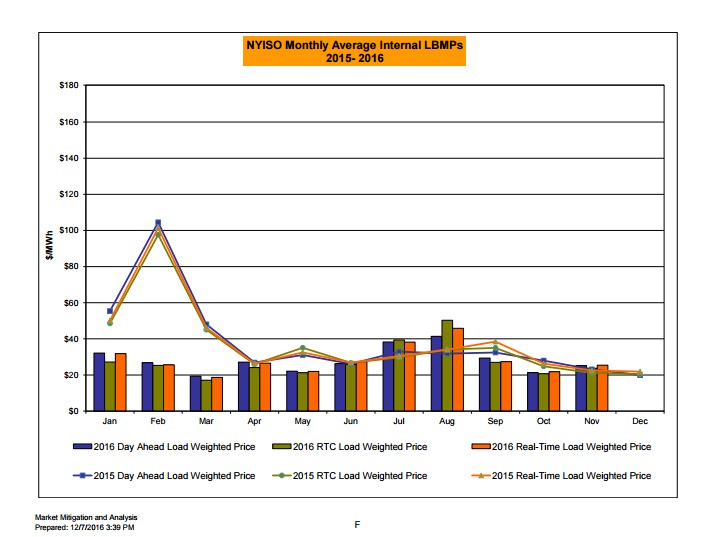

A look at a few of the graphs prepared by the NY ISO in their markets overview from November 2016 underscore the consistently low day ahead and real time prices experienced during 2016.

The following graph compares 2015 day ahead locational based marginal pricing (LBMP, index pricing)– the blue line– to the monthly average for 2016 (the blue bar). Real time prices are depicted by the orange line (for 2015) or the orange bar (2016). Average index and real time prices barely broke the $40/MWh mark across the state during 2016.

These data do not include information from the month of December, although it is clear from MWh’s review of NY ISO December data that last month continued to be a low cost period, particularly in the index markets.

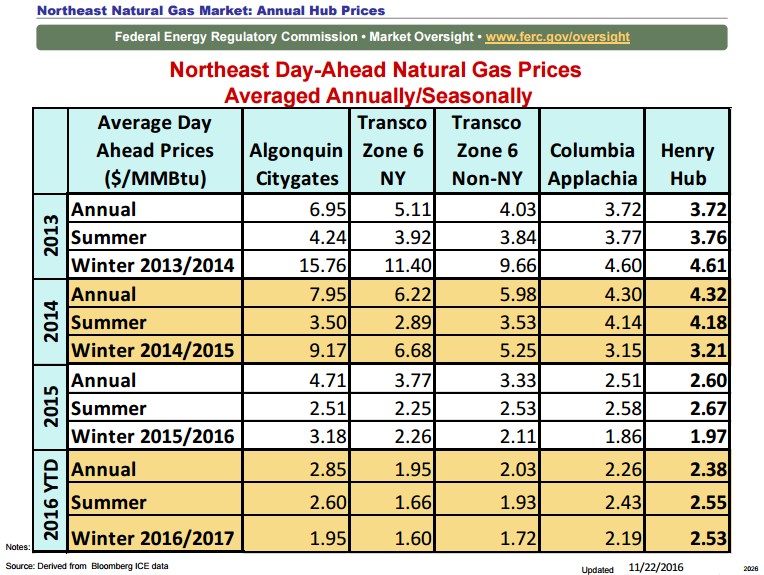

In their review of what to look for this Winter in power and gas markets, FERC reviewed historic pricing data.

The Winter numbers are particularly instructive and helpful in thinking about what to expect in the coming months. Source: FERC

The Winter numbers are particularly instructive and helpful in thinking about what to expect in the coming months. Source: FERC

What to expect in 2017

For those of you who are interested and engaged in energy markets, FERC’s Winter 2016-17

Energy Market Assessment is a thorough review of the current state of markets and what to expect this Winter. Since Winter has become the high cost period in most power and gas markets, and because capacity is generally more than sufficient in most regional markets, Winter costs are the appropriate focus for energy and financial managers.

Power and Gas

FERC’s report is particularly thoughtful on the interplay between gas and power markets. According to FERC summary statement in the report:

Natural gas and power markets are well supplied going into the winter, with plentiful storage, a better-connected pipeline system, and the ability to draw greater imports from Canada through pipelines and higher imports of LNG into New England. However, U.S. natural gas production is down slightly from last year, and prices are likely to be moderately higher than last winter. Most forecasters expect winter temperatures across the Northern U.S. to be average, while most sectors of the gas market should see strong demand relative to last year’s record warm winter. There are challenges though, specifically in regional markets like New England and California, where operational issues could create some regionalized gas and power risk.

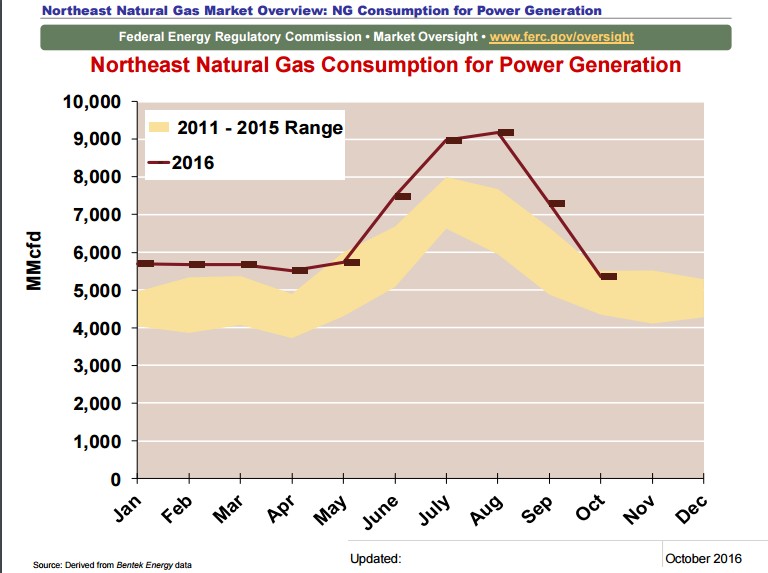

An additional FERC graph tells the story about risk.

We have reported here in the past about the transition to natural gas as a major power generation fuel, particularly in the Northeast. The FERC graph, above, helps to clearly illustrate the significant dependence on natural gas as a power generation fuel in New England.

Going into the winter, natural gas prices are likely to be higher than last year. A warm summer and a small drop in natural gas production resulted in natural gas prices at the Henry Hub increasing from below $2.00/MMBtu in May to more than $3.00/MMBtu in October. An increase in the futures curves for both power and natural gas mirrors cash markets, with many points above year-ago levels and the strongest gains in the Midwest and West Coast markets….The exception to these increases is in New England, where winter basis for both gas and power is down from 2016, due in part to new gas pipeline capacity that will allow more supply to flow into the market area. New York City prices are unchanged, as pipeline constraints into the city keep it the highest priced natural gas market in the U.S. (Source: Winter 2016-17 Energy Market Assessment)

Bottom line for energy buyers and financial decision makers: While energy markets remain relatively tame, it is best to plan and manage energy cost and risk, particularly through the Winter months. Planning ahead is particularly important so as to avoid volatile price periods.