An understanding of the status of NY Energy Markets (both energy and capacity) is essential to planning and managing energy costs. Both short term and longer-term forward prices impact customers as you plan your budgets and forecast your costs.

Why focus on power and capacity? While, electricity supply costs are comprised of a range of components, 70% of your costs are determined by power and capacity costs. Understanding the market dynamics of both components will enable you to plan more effectively.

Capacity and power market dynamics

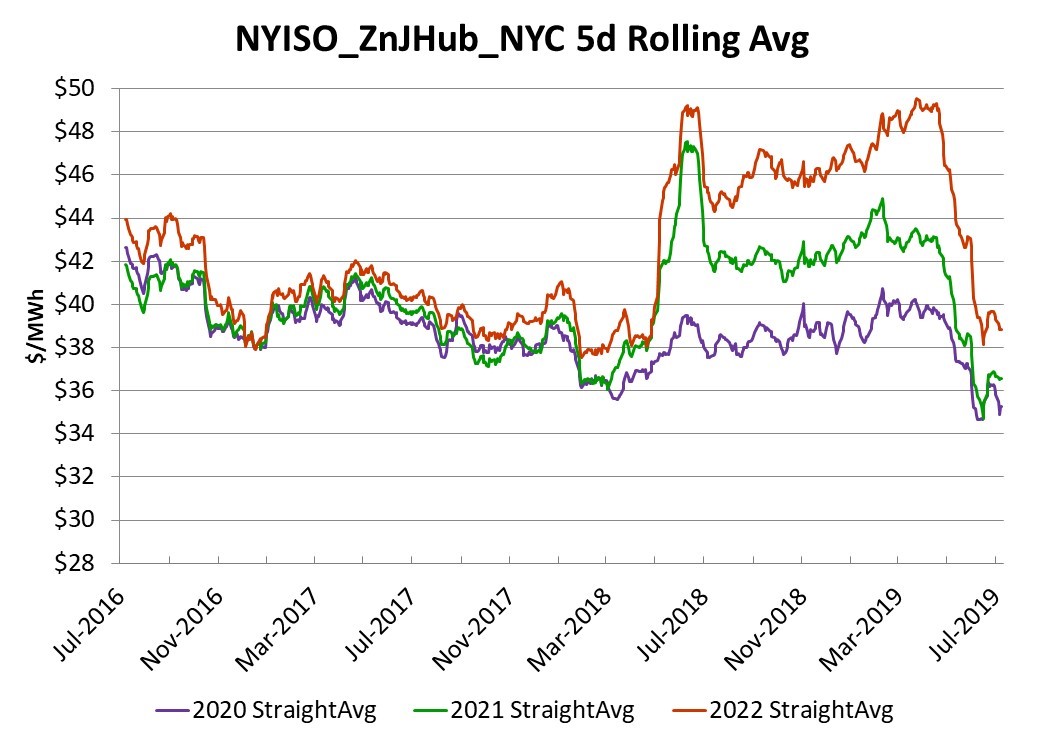

Power markets had been relatively benign and flat for several years in NY State. Then, last Spring (2018) and early Fall, forward markets became more volatile and a bit less predictable, particularly for the years 2022 and 2023.

A comparison of forward power market price movement for the next several years demonstrates the volatility we’re describing. The average forward price in Zone J dropped as much as $14/MWh over the past few weeks.

Why should customers care about this forward market reduction?

Customers who are looking to plan or who are inclined to remove some exposure to future power prices would be wise to consider taking advantage of this market movement. Customers who care most about ensuring they have budget certainty should consider purchasing some component of their electricity supply when market prices decline to these levels. The NY City market has seen prices well in excess of $50/MWh in the past. Market prices below $35-40/MWh represent an important buying opportunity.

Index Prices

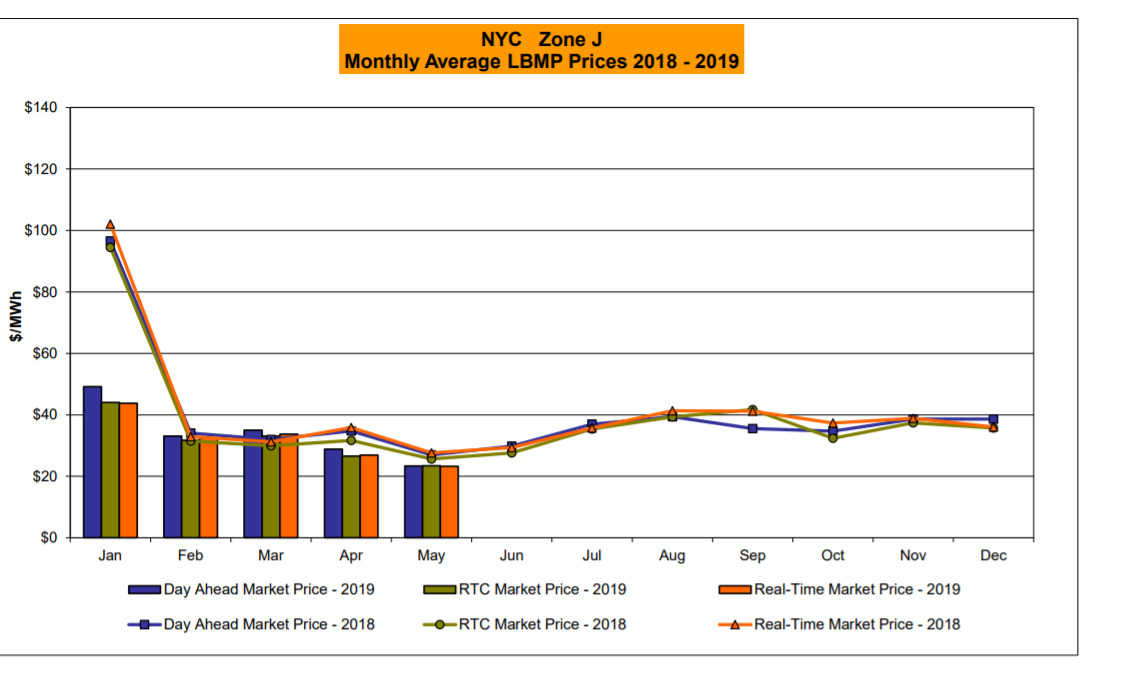

For customers who have some exposure to (day ahead) index prices, these markets have also been low and relatively lacking volatility. The following picture shows 2019 index prices (in bars) compared to 2018 index prices.

Index prices across the State of NY have been low for much of the year.

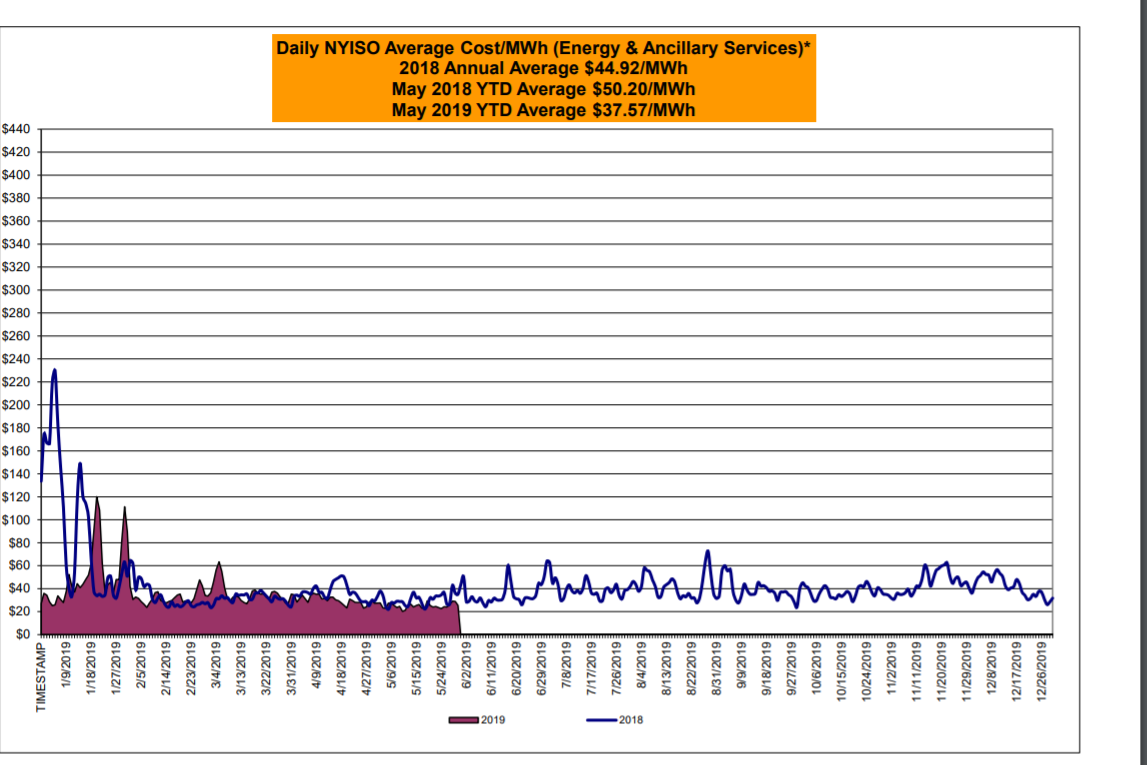

Day ahead markets across the state were lower through May 2019 (purple graph- YTD average $37.57) compared to May 2018 (blue line 2018 to-date avg $50.20). Customers who have either index exposure or who have chosen to remain with their utility for supply in NY will have paid the day ahead index price. Note that while index prices have been low during this calendar year, any customer who chooses to receive index energy will not be able to ensure budget certainty. For example, index prices in January 2018 were high and volatile. In January 2018, index energy customers would have paid as much as $220/MWh and their budgets could been significantly impacted by these power rates.

Capacity prices

Depending on your location, up to 20% of your costs are determined by the cost of capacity. Each electric account is assigned a capacity obligation and each electricity supplier (no matter whether you take electricity supply from your utility or from a retail supplier) must purchase installed capacity to meet that obligation. The market price is set by annual and/or monthly auction processes that differ among the ISOs. This cost will be the second largest component of your electricity cost. (There is no installed capacity obligation or cost in ERCOT.) For more definitions and helpful resources, see TheMWh’s Resources page.

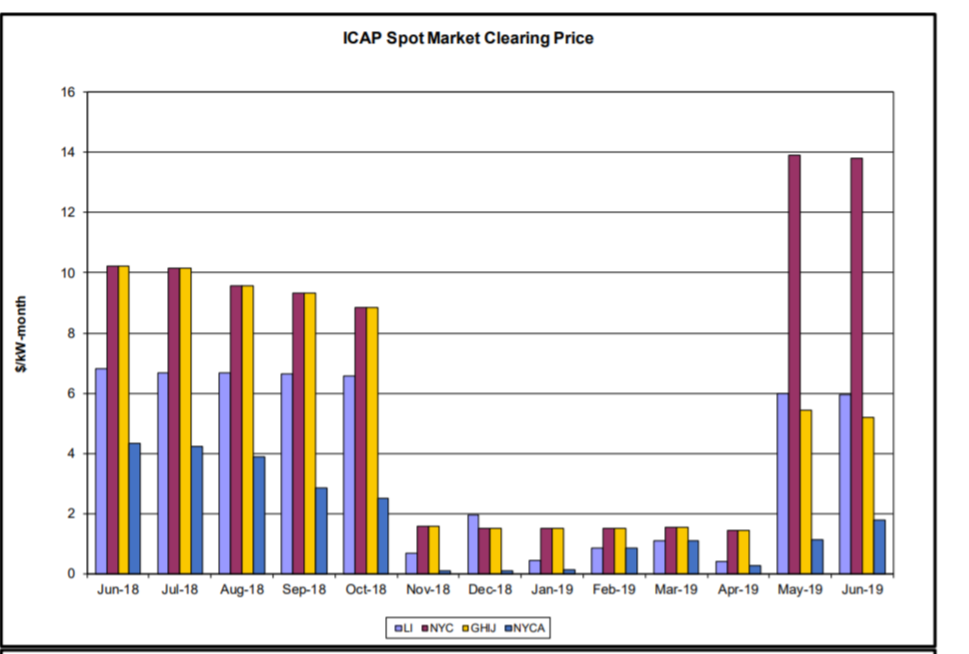

Capacity costs have also been low across the State of NY for several years. In the Fall of 2018, however, NYC summer capacity prices in the forward market increased from $8/kW month to $14/kW month, almost doubling prior year prices. See the graph below, published by the NY Independent System Operator (ISO) for a record of spot market clearing prices from June 2018 through June 2019 across the state. Note that NYC market clearing prices have increased over the past few months while capacity costs elsewhere have declined.

Bottom line for customers: The only way to properly manage energy costs is to have insight into forward costs for power and capacity. It is easy to be lulled into complacency when markets are low and not volatile. However, there is no guarantee that markets will continue to be low and easy to manage and navigate. Keeping an eye on costs over the next one to three years will enable customers to manage energy costs.